There are two major legislative changes occurring today in the banking industry both aimed at making things much more competitive and allowing new businesses to enter and compete with the traditional Big 4 UK banks in the provision of financial services. Underpinning both of these initiatives is the desire to ensure that customers garner a better understanding of their financial position as well as providing those same customers with the necessary knowledge to make better informed financial decisions. Helping them to get the best value from their money; whether that’s maximising the return on an investment or minimising the interest accrued on an overdraft or loan:

Open Banking

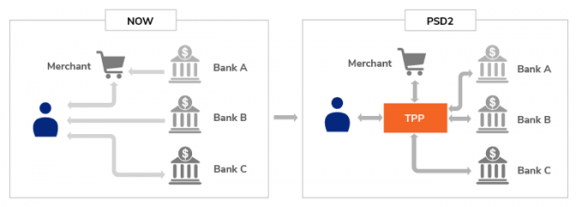

A new secure method by which consumers, be they personal account customers or small to medium sized businesses, can provide access to elements of their financial data to identified third party providers (TPP’s). This facility is already live and available to anyone with on-line and/or mobile banking. It’s a UK Government initiative introduced by the Competition and Markets Authority and provides the ability to make payments.

PSD2

This is the latest iteration of the Payments Services Directive and is a Europe-level initiative to better regulate payment services and payment service providers throughout the EU (including SEPA). One of its primary purposes is to open up access to the payments market to “non-banks” as well as harmonise the legal obligations for payment providers and users.

PSD is split into two areas:

- Market Rules describe who can provide Payment Services including Credit Institutions (banks), government bodies, central banks and a new category of “Payment Institutions”.

- Business Conduct Rules describe the mechanics and returns expected from both Credit and Payment Institutions.

Open Banking Within the UK

In the UK we have seen the introduction of ‘Open Banking’ where the traditionally insular barriers to a person or company’s financial history can be opened up to approved TPP’s, providing the consumer is happy to provide that visibility.

This controlled access is a much more sophisticated (and safer) method of sharing financial data than the ‘screen scrape’ approach previously used for harvesting a user’s financial affairs once their user name and password had been shared. Under Open Banking the user’s data is secure and there’s no risk as user names and password details are never shared.

The impact of this initiative has been to open up banking to non-banks and increase financial competition. This is revolutionising the way we bank, and our banking habits will continue to undergo dramatic change as customers use technology to derive better understanding and value from their banking rather than just limiting their options to the products offered from the traditional vendors.

The Banking opportunities created by these new changes

The ability for different financial systems to interact and exchange data has been available for many years but is only now being seen across the banking industry. Underpinning this change has been the introduction of a large number of standardised banking interfaces (APIs) allowing banking organisations to better share data through the introduction of standardised mechanisms, formats and controls designed to facilitate the efficient and economic operation of Open Banking.

Examples of these new initiatives are already being seen in the Financial Services and Mortgage sectors:

- Financial Services– Today you are able to make choices not only about who your Financial Services provider(s) are but whether you want to make certain details of your financial history available to that provider or specialist third party providers. With Open Banking many institutions/web-sites are offering a portal facility incorporating dashboards where you are able to review not only your bank account(s) across a number of banks but also how your pension and other investments are performing.

- Mortgage sector– Currently when applying for a mortgage you have to provide proof of earnings/income. Traditionally, this could be achieved by taking the last 3 pay slips and sharing these with your prospective mortgage provider. Today, through Open Banking, you can now provide competing mortgage provider(s) with access to view elements of your current account and can evidence your salary and employment details in a matter of seconds to secure the best current offers. New entrants to the market now offer these and other ground-breaking services.

We have seen the introduction of entirely new services covering everything from the electronic creation of electronic receipt details for contactless transactions to the introduction of new services allowing new competitors to break into previously heavily regulated banking processes such as peer-to-peer lending. New companies have been able to develop more innovative comparison web-sites which can help secure the best deal for the individual supporting a much more bespoke banking service being offered to tech savvy consumers.

Oracle’s approach to the Banking Sector

Oracle is also making its own contribution to this space with the announcement of the introduction of a series of banking API’s designed to better enable connectivity between banks, other financial services providers as well as the new Fintech entrants to the market.

The integration and communication rests on the introduction of 1500 API’s which Oracle has spent 20+ years developing and are now available to underwrite the integration requirements of Open Banking.

For organisations planning to take advantage of these new market opportunities being able to easily access and adopt these API’s or even to develop new ones is key to securing their competitive advantage.

Oracle has developed these 1500+ pre-built RESTFul banking API’s now available on Swagger, along with extensive documentation allowing the fastest possible time to market providing instant integration not just for the established banks but for the new fintech entrants supporting innovative new products and services.

The Oracle solution for Open Banking (Diagram 1.1) offers complete API management from standardisation, design, documentation, security to discovery, consumption, monetizing and analysis ensuring smooth and easy digital transformation for banks and fintech entrants.